The State Pension serves as a valuable foundation for your retirement income and can significantly enhance your financial stability in later life.

Pensioners in receipt of the full UK State Pension will typically receive £11,502 for the 2024/25 tax year (rising to £11,904 in 2025/26).

To qualify, you need to have made 35 years of National Insurance contributions (NICs). If you’ve made fewer than this, your State Pension will be smaller.

You have until 5 April 2025 to pay voluntary contributions to make up for gaps between April 2006 and April 2016. After 5 April 2025, you’ll only be able to pay for voluntary contributions for the past 6 years. So, acting now to address any gaps in your record could significantly boost your retirement income.

Read on to discover how much extra you could receive by topping up your State Pension before the upcoming deadline.

You need at least 10 qualifying years of National Insurance contributions to receive a State Pension

To qualify for the minimum State Pension, you must have at least 10 years of NICs on your record, while 35 years are required to receive the full amount. If your contributions fall between 10 and 35 years, your State Pension will be calculated proportionally, meaning you’ll receive a reduced amount based on the number of qualifying years you have.

You make NICs by:

- Paying National Insurance (NI) on your income or earnings

- Making voluntary contributions (most popular for non-UK residents)

- Receiving NI credits, which you can get if you’re signed off work sick, claiming unemployment benefits, or caring for a relative.

If you took time off work and didn’t claim credits or there was a period in your career when you didn’t earn enough to pay NICs, you may have gaps in your record.

You can check your State Pension forecast to find out how much you can expect to receive based on your existing record.

If you haven’t made the full 35 years of contributions, you can still buy credits to fill any gaps dating back to April 2006

If you’re nearing retirement and you’re worried you haven’t made enough contributions to receive the full State Pension, you can buy credits to fill any recent gaps.

Normally, credits only cover the past six years. However, until 5 April this year, you can buy credits to plug gaps in your record dating back to April 2006, provided you reached or will reach State Pension Age after 2016. After 5 April 2025, the normal six-year limit will apply.

The original deadline for this backdating extension has already been changed twice as many people felt there wasn’t sufficient time to make additional contributions. This means that while you still have time to fill in any gaps in your record, the current date is unlikely to be changed again.

So, it’s a good idea to make additional contributions while you can to boost your State Pension and optimise your retirement income.

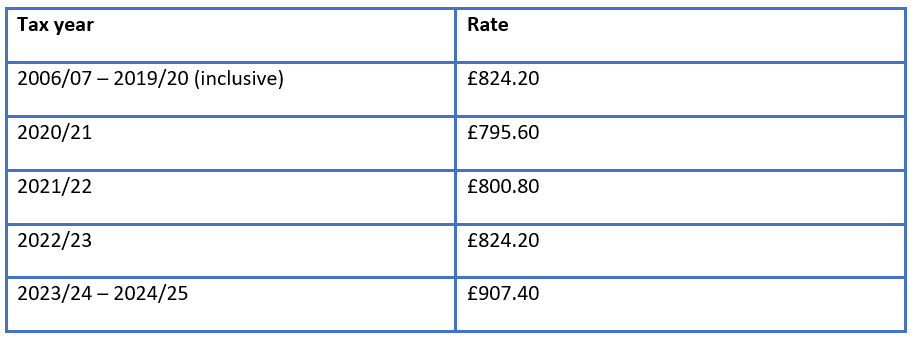

The cost of topping up your contributions depends on the tax years you missed

It costs money to fill in gaps in your NICs and the full rates vary depending on the tax year you missed. You may also pay a slightly lower rate if you made some contributions that year, but not enough for it to qualify as a full year.

The table below shows the cost of topping up your NICs for different tax years. It’s important to remember that the cost may be different if you’re self-employed.

Source: PensionBee

Standard Life calculates that buying credits for any of the tax years between 2006/07 – 2019/20 (inclusive) or 2022/23 for £824.20 could boost your State Pension by £275.08 a year.

This means it would only take around three years of receiving your State Pension to make your money back. Indeed, if you start receiving your State Pension at 66 and live for another 20 years, your £824.20 investment could add around £5,500 to your total retirement income.

So, buying credits to fill the gaps in your record could offer a significant return on investment over the course of your retirement.

A financial planner can help you determine if buying additional credits is the right choice for you

Your income is an integral part of your retirement plan, at home or overseas. So it’s a good idea to keep your financial planner informed about your State Pension.

While topping up gaps in your NI record can be a good move in preparing for retirement, it’s not always the right choice for everyone, depending on their health, age, and sources of income.

A financial planner can work with you to assess your options, and help you find the best strategies for building your retirement savings and ensuring your income supports your long-term goals.

To speak to a financial planner, get in touch.

Email contact@ambient-wm.com or call us on +34 658 077 450.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.