In many walks of life, people often stick to what they know out of loyalty, habit, or even fear.

You may have a supermarket you always shop from, a destination you frequent for your holidays, or a particular dish you never fail to order from your favourite local restaurant.

There can be a sense of comfort within the familiar, while you may be more hesitant about venturing into the unknown.

While this can make sense in certain situations, when it comes to your investments, sticking to what you know could actually lead to more risk and less growth compared to broadening your horizons.

“Home bias” refers to the tendency for investors to favour investments in their home country. Although this might feel comfortable, it can mean missing out on the benefits that an internationally diversified portfolio can bring, such as reduced risk, and the potential for stronger long-term returns.

Read on to find out how having a home bias could hold back your portfolio.

Home bias exists for multiple reasons

There are several reasons why investors often exhibit a home bias.

Some may be psychological. For instance, you might feel that your knowledge of the domestic market gives you an edge, or you may think foreign assets are riskier and prefer the familiarity of home markets.

Other factors might be more technical. Differences in regulations, taxes, and transaction costs can make international investments seem less attractive.

Moreover, if you have investments you rarely touch, you may inadvertently have a home bias even as global markets evolve. This is especially relevant for UK investors, because the UK market now represents a much smaller share of global equity than it did in previous years.

Home bias risks leaving you overexposed

Having a home bias can mean that your portfolio is left exposed to the economic performance of the region you favour. While market dips can sometimes be felt around the world, they can also be regionally contained and based on local events.

For example, if you have a British home bias and the UK economy faces a downturn, the value of your portfolio could drop as domestic businesses struggle. This could have happened in 2022, when the UK market dipped after the announcement of the mini-budget.

By contrast, a globally diversified portfolio can help smooth out volatility. While UK shares may have fallen, investments in other markets could have risen, helping to maintain the overall value and balance of the portfolio.

Moreover, a report in FTAdviser found that 25% of the average UK balanced portfolio is invested in the UK. However, the UK accounts for only 3% of global GDP and 4% of global equity and bond markets, meaning the average portfolio is missing out on growth opportunities further afield.

A globally diversified portfolio can help maintain stability and capture growth

While a home bias can leave you open to risk and overexposed, a globally diversified portfolio is more likely to remain stable during periods of volatility and is better positioned to capture growth.

The FTAdviser report notes a study that looked at the returns on £10,000 invested in the UK market between 2003 and 2022. It found that returns would have been considerably different depending on the level of global diversification in the portfolio.

A portfolio with 100% domestic investments, a full home bias, would have returned £31,472. Meanwhile, a portfolio with 100% global investments would have returned £43,276 over the same period. This shows how concentrating your portfolio can mean you miss out on wider growth.

When it comes to maintaining stability, the varied performance of global markets shows why it’s a good idea to avoid a home bias.

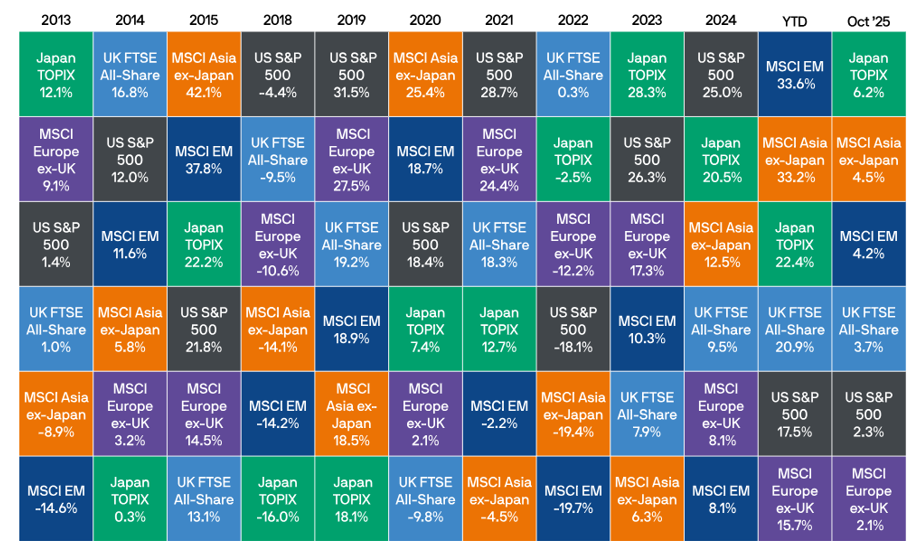

The chart below shows the ranked performance of major global markets from 2013 to October 2025.

Source: JP Morgan

As you can see, predicting which markets will perform well based on the previous year’s ranking is all but impossible, and being overly invested in one region could cause your portfolio to fluctuate wildly.

For example, if you had all your investments in the UK in 2020, you would have missed out on the huge growth of the MSCI Asia. However, being overly exposed to the MSCI Asia would have meant you’d drop considerably the following year.

This kind of volatility highlights the risks of concentrating your investments in a single region or market. When your portfolio is heavily tied to one area, you’re more exposed to local economic shocks and market swings.

By contrast, spreading your investments across different regions can help cushion you against downturns in any one market while giving you the opportunity to benefit from growth elsewhere.

A financial planner can help you diversify your portfolio and reduce home bias

A financial planner can help you identify and correct a home bias in your portfolio.

They can assess how much of your portfolio is tied to one economy and model how different levels of global diversification might affect your long-term returns and volatility. They can also ensure that your strategy is implemented in an efficient and cost-effective way.

In short, a financial planner can help you move beyond a home bias and build a portfolio that is better protected and positioned for long-term growth.

To speak to a financial planner, get in touch.

Email contact@ambient-wm.com or call us on +34 658 077 450.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.